As of Q3 2020, global default rates surged from low single digits to more than 6% from the lingering impact from the coronavirus against a massive nonfinancial corporate debt burden. CreditRiskMonitor forecasts that these rates will exceed 12% by 2021, and bondholders will incur record-breaking financial losses, half of which have been incurred in recent quarters. Due to debt-heavy capital structures and limited financial covenant protections, companies have delivered record-low recovery rates, particularly for unsecured bondholders and trade creditors.

Trade Creditors Collect Pennies

Despite the trillions in monetary and fiscal policy stimulus aimed to support corporations, default rates and bankruptcy filings are surging anyway, including among the largest public companies. According to CreditRiskMonitor research, about 85% of public companies tend to restructure as opposed to liquidating. Since public companies have loaded their capital structures with revolving credit, terms loans, and bonds, senior creditors absorb most payment claims during restructuring.

According to Bloomberg, credit default swap auctions show that average creditor recovery rates have plunged to cents on the dollar. Over the last decade, bankruptcy restructurings would typically provide unsecured creditors with about $0.30 per dollar owed. However, in 2020, the coronavirus downturn reduced the average recovery to only $0.035 (3.5 cents).

During the court process, creditors and debtors of a given public company are required to agree upon a haircut to outstanding obligations. For example, if the debt capital structure comprises half secured and half unsecured claims, the issuer might historically apply a 20% haircut to the senior position and 70% to the mezzanine debt for an aggregated 45% haircut. During a coronavirus-induced bankruptcy, however, company cash flows and asset valuations have declined substantially and performance resiliency is not a given. Therefore, the aggregated haircut might steepen to 65%, whereby the secured creditors would receive a 35% haircut and the unsecured would absorb a much higher 95% loss compared to the previous example. This scenario is where we stand today. Since trade creditors often sit behind bondholders on the payment priority pyramid, vendors should expect very low recovery rates for the foreseeable future.

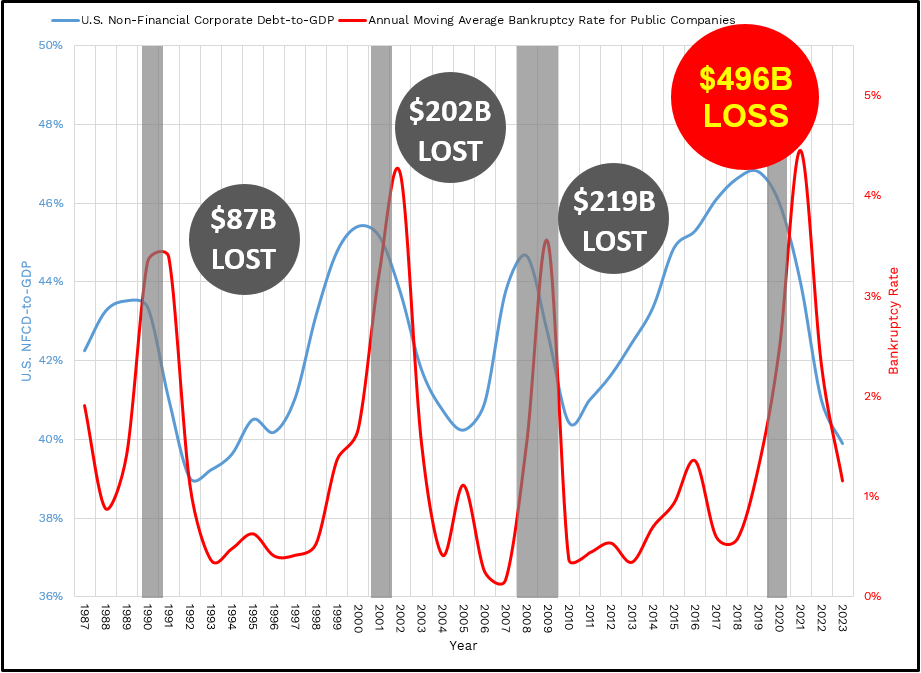

Reported bankruptcy filings are moving more quickly relative to the Global Financial Crisis as well. CreditRiskMonitor’s research shows that public company bankruptcies with FRISK® scores during the six-quarter stretch during the Global Financial Crisis (Q2 2008 to Q4 2009) totaled 195 large corporations. During the first three quarters of 2020, a total of 154 public companies have filed for Chapter 11 bankruptcy, indicating that nearly the same amount of bankruptcies have transpired in half the time. Under current conditions, the public company bankruptcy rate should approach 4.5% by 2021, resulting in nearly $500 billion in financial losses to bondholders.

CreditRiskMonitor research has also found that the average receivable portfolio has 53% dollar exposure to public companies through parent-subsidiary relationships. In 2020, the Federal Reserve estimates that total corporate accounts receivables were $3.5 trillion. If bondholders carry a higher priority of payment in the bankruptcy hierarchy yet are absorbing $500 billion in losses, there’s a reasonable likelihood that most companies will be forced into massive receivable write-downs. However, companies can avoid these consequences by evaluating financially distressed counterparties frequently and implementing timely risk mitigation.

Always Be Looking Forward

With bloated balance sheets, some corporations will be challenged navigating through this turbulent economy and have no choice but to file bankruptcy. CreditRiskMonitor’s FRISK® score gives risk professionals the ability to create a company portfolio that assesses risk in real-time and identifies specific counterparties at risk of bankruptcy within the next 12 months. The FRISK® score uses a “1” (high risk)-to-“10” (low risk) scale, whereby 96% of public companies that eventually go bankrupt are classified in the "red zone", which is the lower half of the range, for at least 3-month period to their filing.

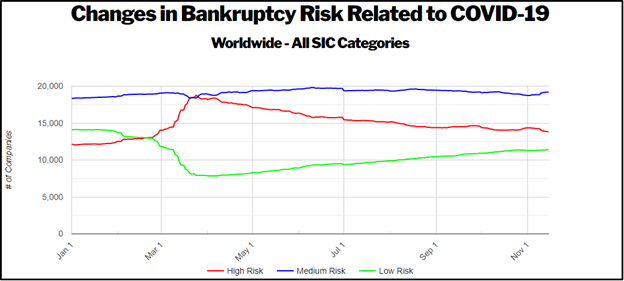

Public company bankruptcies have severely impacted credit and treasury functions as well as crippled corporate supply chains. Both supply and demand shortages have occurred, and certain industries have reported sales slowdowns that have caused cash crunches for manufacturers, service providers, and any cyclical-related industry vendors. Professionals can access our COVID-19 Credit Crisis resources to observe which sectors, industries, and countries are being most affected in this global downturn. The graphics show changes in bankruptcy risk and highlight significantly fewer low-risk public companies worldwide today than before the pandemic.

After that, users can further evaluate industries that are most relevant to their own business by applying the same tools to their specific counterparty portfolio and custom lists.

Bottom Line

As public company bankruptcies continue to unfold, it’s never been more important to monitor counterparty financial risk. With excessive corporate debt and rock bottom recovery rates, this downturn has created a perfect storm for financial losses to unsecured creditors, particularly trade vendors. Supply chains are also experiencing remarkable disruptions and subdued demand in their end markets. Furthermore, not only will public company bankruptcy filings reach an all-time high of 4.5%, they will likely remain elevated for at least the next few years.

Interested in learning more? Contact CreditRiskMonitor to identify your riskiest customers and suppliers today.